In the past year, discussions of inflation have intensified as the cost-of-living increases. Many in the general public are experiencing increased food and other general living expenses without increasing wages at the same time. There are many nuances when discussing inflation and what causes it.

Inflation is a distraction from the real problem with money backed by governments.

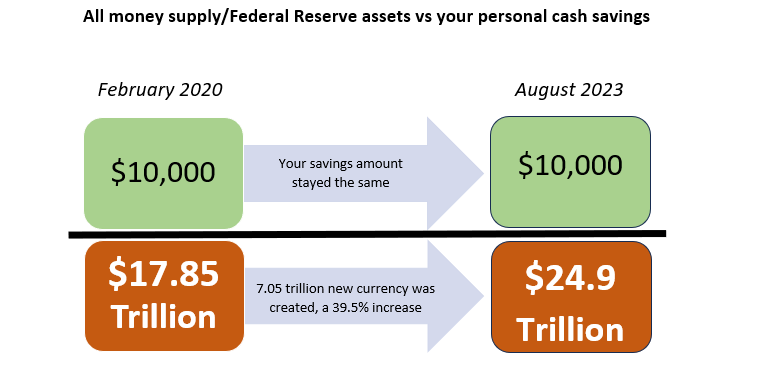

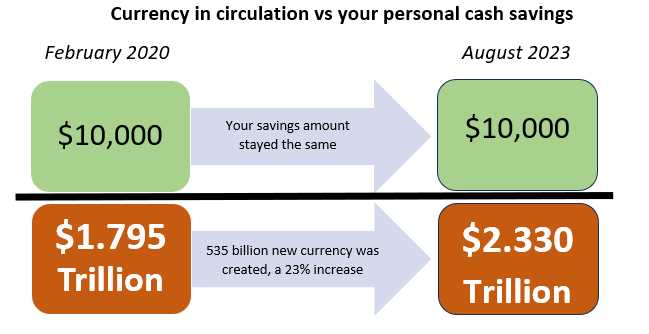

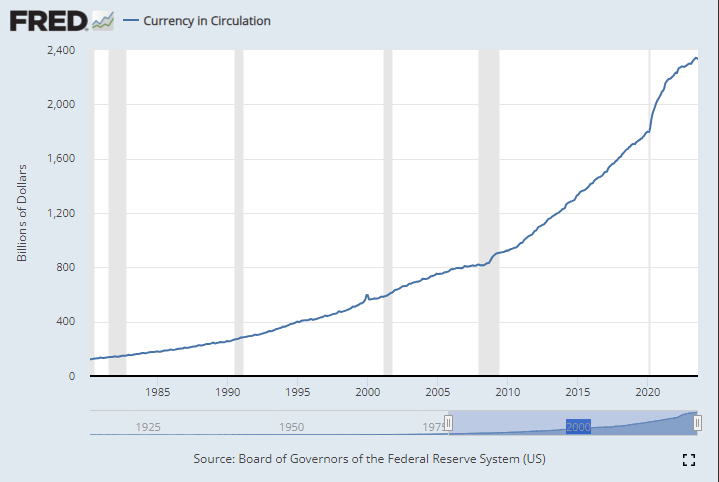

The real problem with money backed by governments is its ability to debase the currency. Debasement is easy to understand if its visualized. Imagine you have $10,000 in your savings account; depicted below as the numerator. The purchasing power of your savings account is based on how much currency is in circulation. The denominator is the amount of currency in circulation today.

In the last 3 years, 23% more currency was created, that means your savings lost 23% of its purchasing power.

Here I’m showing the amount of currency as the metric to convey the concept of debasement. Some who understand the banking system and how the plumbing works for money in relation to banks, governments and debt will say that just looking at currency in circulation is not the full story. The new currency is allocated by the banks and governments based on spending bills passed by congress. New money spent on agriculture keeps food prices lower while new money spent on more controversial spending takes longer to hit consumer prices due to the nature of the spending.

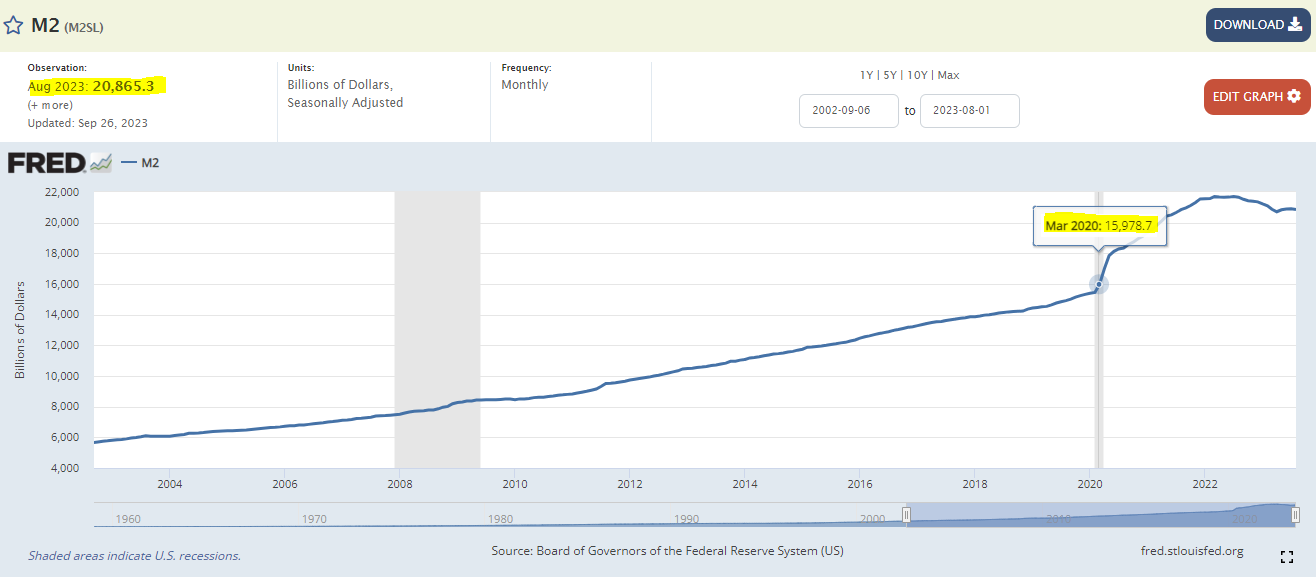

Regardless of what other information is presented, the trend over the past 30+ years has been the creation of new money by different organizations including banks via loans and governments via debt so that goods and services can be purchased today and paid for over time. Both of these add to the supply of money in the system; hence increasing the denominator of the above illustration.

The only thing to focus on is that, more debt and money in the system means the money you have in savings loses its purchasing power. This is debasement, it allows the person who takes out loans or debt the advantage of purchasing assets today and paying for them over time with money they earn years later at higher pay rates from their job.

Banks are the creators of money and when the Federal Reserve provides liquidity to prevent their failure, a direct debasement of currency occurs.

During the banking holiday of 1933 the rules changed for banking, most notably the ability for the federal reserve to create dollars without the backing of gold. The idea being that the assets of the bank can be used to back any new dollars that are created. Between then and now, banks today can loan money without assets backing the loans. Read directly from the U.S. Federal Reserve website how reserve requirements are currently 0% but were previously between 3% and 10%.

Banks play an important role by providing credit to entrepreneurs, both to those who pledge assets to back the loan or by taking a risk that the business plan will produce profits. If you put up your land as collateral for a loan, and you do not make the payments, the bank will take your land. However, if the bank loans you money on your business idea and it fails, the bank should be able to absorb the loss. If the loss is so great that it affects the operation of the bank, the FDIC will take over the bank guaranteeing bank deposits and work to sell the remaining bank assets and operations to other banks.

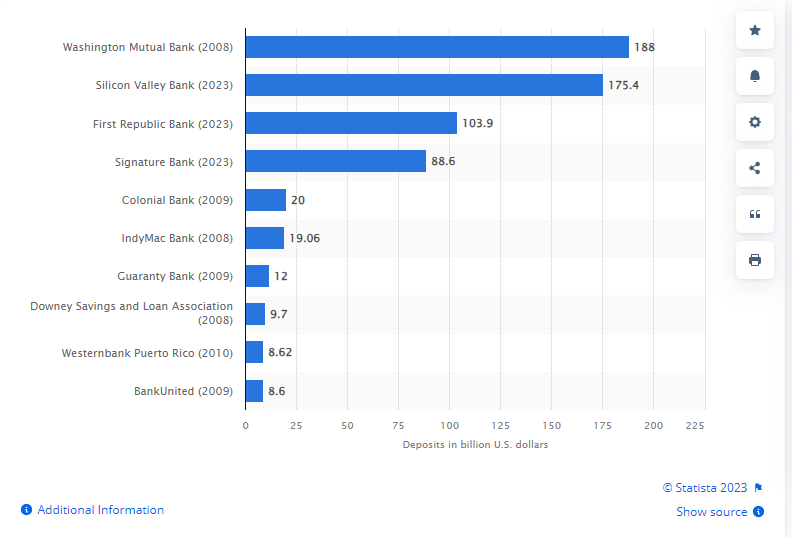

If the failure becomes systemic, meaning a domino of other banks begin to fail, the Federal Reserve will stand in as the lender of last resort by providing liquidity to keep the banks operating. During the great financial crisis of 2008, the federal reserved did just that to keep banks afloat by creating a new “mechanism” to provide liquidity. In March of 2023 when First Republic bank and others began failing, the Federal reserve opened a new liquidity “mechanism” called the bank term funding program (BTFP) in addition to already existing liquidity mechanisms. The BTFP was designed to allow banks to receive dollars for bonds they purchased which have lost value due to the recent interest rate hikes. By providing them liquidity using BTFP, banks are not at risk of failure due to bank runs, i.e. people withdrawing their money. These banks from March 2023 failed because they could not sell their bond assets to cover people withdrawing funds. These bonds went “no bid” meaning nobody wanted to buy bonds paying 1% interest when they can get 5% elsewhere.

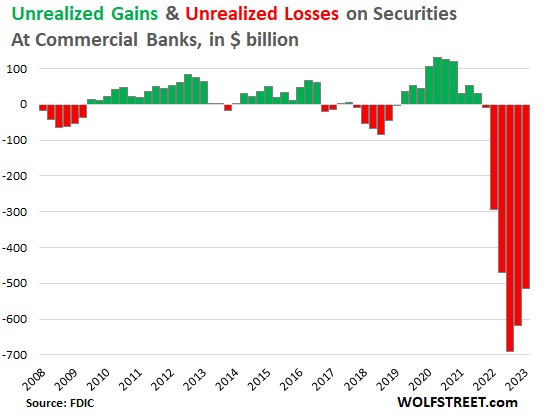

The current problem of bond losses is growing. The main reason this is occurring is because these bonds were purchased when interest rates were significantly lower and when interest rates rise, the price “value” of the bond falls.

How did we get into this situation where we could see another thousand banks fail in the next 5 years?

“Never let a crisis go to waste.” is an old catch phrase which jives well with creating this situation. During the pandemic and the subsequent lockdowns, the federal reserve signaled to the market that rates would remain low. Many banks were flush with cash from stimulus payments. Those dollars cannot just sit on banks balance sheets, they need to “invest” those dollars to pay operating expenses. When there is excess cash, banks purchase government securities, a.k.a treasury bills a.k.a bonds. This is exactly what many banks did with excess cash, and today these banks are teetering on the brink of bankruptcy if any slight bank run starts on them.

The bank failures in March 2023 were larger in than 2008.

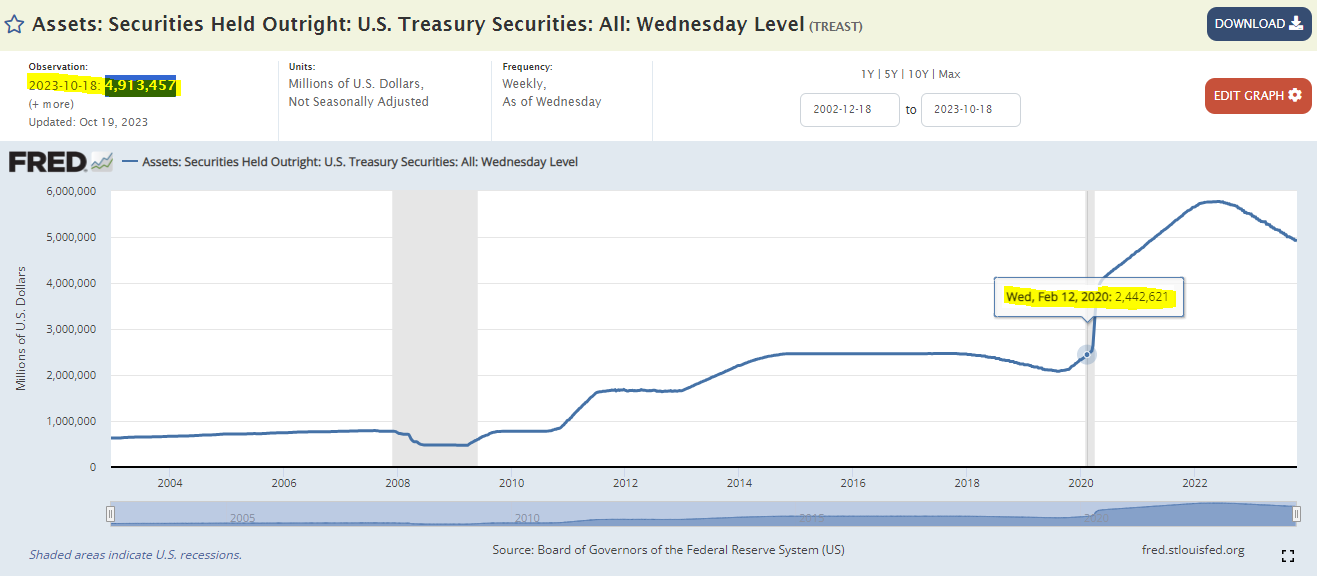

So how does this relate to debasement? When the Federal Reserve needs to provide liquidity, they buy government securities from banks with new currency.

That clip from Jerome Powell is from 2020 when the Federal Reserve created a series of new liquidity mechanisms for the market. New “mechanisms” and “facilities” were created to save a larger swath of the economy. One of these facilities saved the junk bond market. I remember it clearly as one of my holdings was high yielding junk bond funds. During the market crash, much of the value evaporated only to return shortly after, you can see 3 popular funds crash and recover below.

iShares Broad USD High Yield Corporate Bond ETF | Google Finance

SPDR Bloomberg High Yield Bond ETF | Google Finance

Fidelity High Income Fund | Google Finance

The idea of the Federal Reserve being the lender of last resort for all of the banks and financial institutions allows it to debase the currency at the expense of everyone who uses it. This is where bank losses end up going, poor decisions made by banks and other financial institutions are absorbed by everyone.

The U.S. government allows this to occur mainly because much of the securities being “absorbed” by the federal reserve during these crises are from government bonds issued to fund itself.

If we now include all federal reserve facilities as part of the total money supply, we can get a better picture of how much debasement is really occurring during the same time period of February 2020 to today. Including all of the additional currency being created, we were debased by 39.5% in the last 3 years alone!